Profit Maximization

Christopher Makler

Stanford University Department of Economics

Econ 50 : Lecture 16

pollev.com/chrismakler

What color shirt am I wearing?

Today's Agenda

- Review of short-run costs

- Revenue as a function of \(q\)

- Profit as a function of \(q\)

- Everything this week is in the short run.

Theory of the Firm

Labor

Firm

🏭

Capital

⏳

⛏

Customers

🤓

p

w

r

q

L

K

Firms buy inputs

and produce some good,

which they sell to a customer.

PRICE

QUANTITY

Labor

w

L

Capital

r

K

Output

p

q

Firm

🏭

Costs

wL + rK

Revenue

pq

Theory of the Firm

Firms buy inputs

and produce some good,

which they sell to a customer.

PRICE

QUANTITY

Labor

w

L

Capital

r

K

Output

p

q

Costs

wL + rK

Revenue

pq

Profit

\pi = pq - (wL + rK)

Next week: Solve the optimization problem

finding the profit-maximizing quantity \(q^*\)

The difference between their revenue and their cost is what we call profits, denoted by the Greek letter \(\pi\).

Theory of the Firm

Costs

c(q) = wL(q) + rK(q)

Revenue

r(q) = p(q) \times q

Profit

\pi(q) = r(q) - c(q)

Theory of the Firm

Our approach will be to write costs, revenues, and profits all as functions of the ouput \(q\).

Profit

\pi(q) = r(q) - c(q)

Theory of the Firm

Our approach will be to write costs, revenues, and profits all as functions of the ouput \(q\).

We will then just take the derivative with respect to \(q\)

and set it equal to zero to find the firm's profit-maximizing quantity.

\pi'(q) = r'(q) - c'(q) = 0

r'(q) = c'(q)

MR

MC

Theory of the Firm

L^*(w,r,q)

K^*(w,r,q)

Exogenous Variables

Endogenous Variables

technology, \(f(L,K)\)

level of output, \(q\)

input prices \(w, r\)

Cost Minimization

Profit Maximization

cost function, \(c(w,r,q)\)

revenue function \(r(q)\)

\text{Optimal Output }q^*

Friday

Monday

Wednesday

Firm Production Functions and Cost Minimization

Profit Maximization

Input and Output Decisions of a Competitive Firm

Unit III: Theory of the Firm

Week 6

Week 7

Checkpoint II

Cost Functions

and Cost Curves

Elasticity and Market Power:

From Monopoly to Competition

Monday

Checkpoint III

Week 8

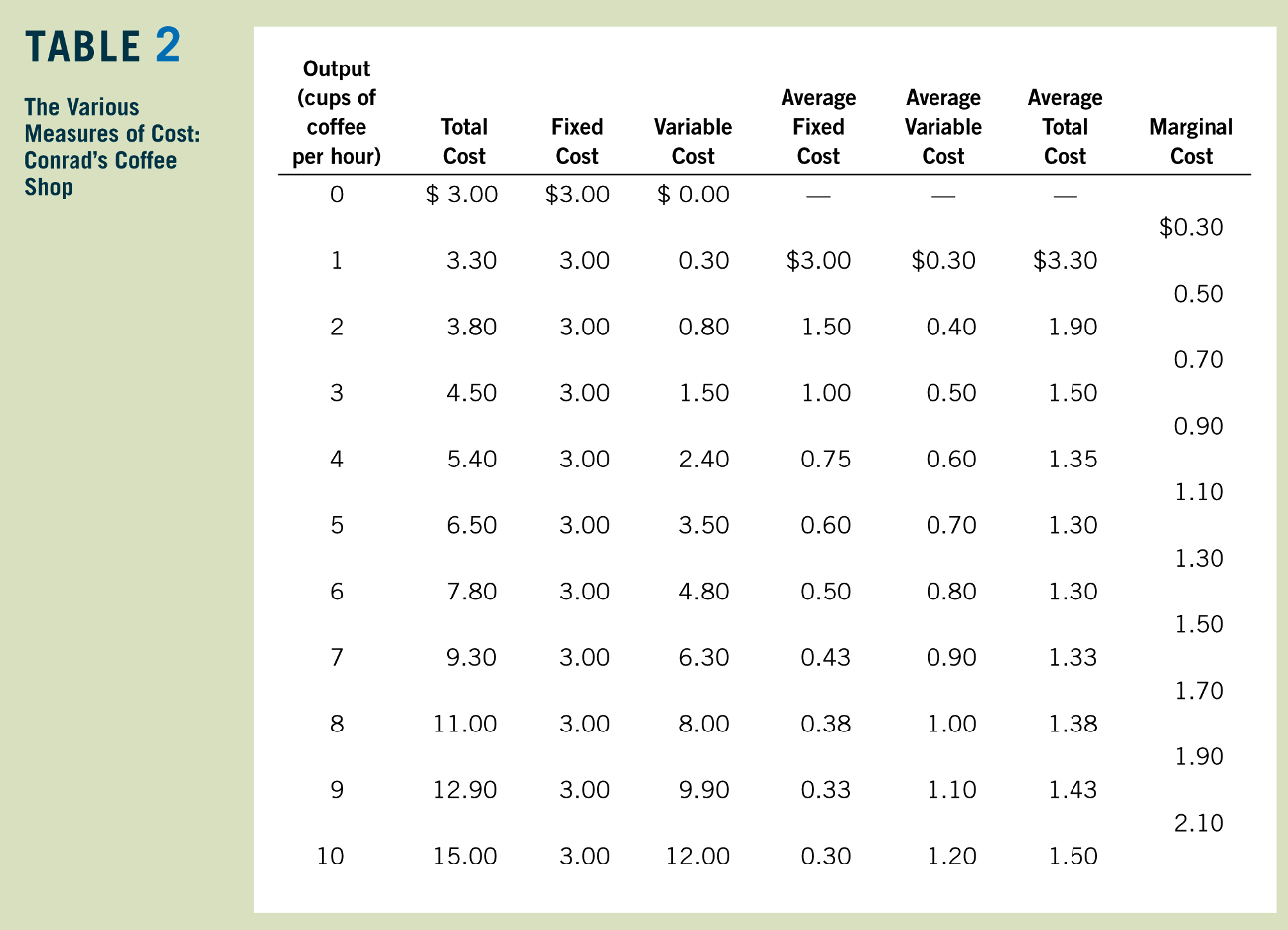

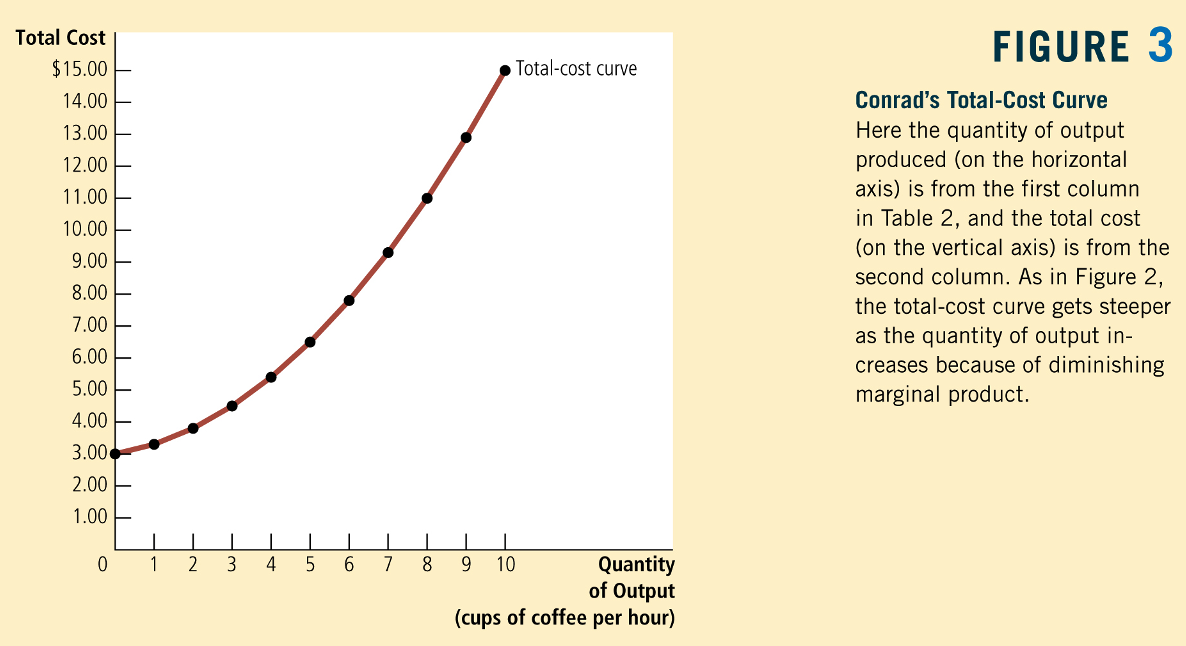

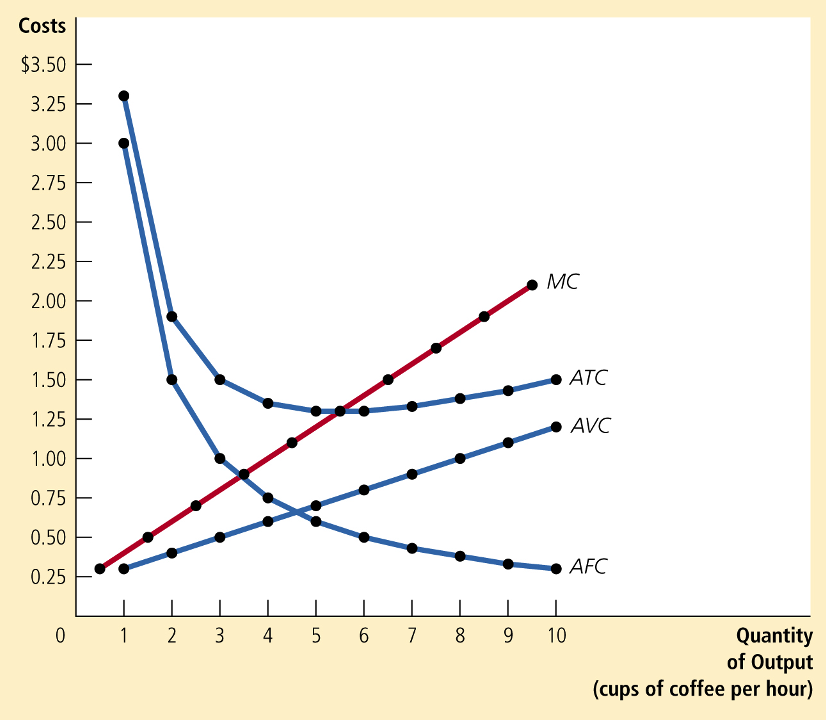

Review: Short-Run Costs

Greg Mankiw, Principles of Economics

Greg Mankiw, Principles of Economics

Dollars

Dollars Per Unit

Now assume that the level of capital is fixed in the short run at some amount \(\overline K\).

q = f(L\ |\ \overline K)

The amount of labor required to produce \(q\) units of output is therefore also going to depend upon \(\overline K\):

L(q\ |\ \overline K)

Short-Run Total Cost of \(q\) Units

TC(q\ |\ \overline{K}) = wL(q\ |\ \overline{K}) + r\overline{K}

Variable cost

"The total cost of producing \(q\) units in the short run is the variable cost of the required amount of the input that can be varied,

plus the fixed cost of the input that is fixed in the short run."

Fixed cost

f(L,K) = \sqrt{LK}

Short-run conditional demand for labor

if capital is fixed at \(\overline K\):

Total cost of producing \(q\) units of output:

L(q\ |\ \overline K) = {q^2 \over \overline K}

c(q\ |\ \overline{K}) = wL(q\ |\ \overline{K}) + r\overline{K} =

{wq^2 \over \overline K} + r\overline K

Example: \(w = 8\), \(r = 2\), \(\overline K =32\):

TC(q) = 64 + {1 \over 4}q^2

\text{Total Cost}: TC(q) = F + VC(q)

\text{Average Cost}: ATC(q) = \frac{TC(q)}{q} = \frac{F}{q} + \frac{VC(q)}{q}

Fixed Costs

Variable Costs

Average Fixed Costs (AFC)

Average Variable Costs (AVC)

Average Costs

\text{Total Cost}: TC(q) = F + VC(q)

\text{Average Cost}: ATC(q) = \frac{F}{q} + \frac{VC(q)}{q}

Average Costs

TC(q) = 64 + {1 \over 4}q^2

ATC(q) = {64 \over q} + {1 \over 4}q

\text{Total Cost}: TC(q) = F + VC(q)

\text{Marginal Cost}: MC(q) = TC'(q)

Marginal Cost

TC(q) = 64 + {1 \over 4}q^2

MC(q) = {1 \over 2}q

Relationship between Marginal Cost and Marginal Product of Labor

TC(q) = wL^c(q | \overline K) + r \overline K

{dTC(q) \over dq} = w \times {dL^c(q) \over dq}

= w \times {1 \over MP_L}

Revenue

Profit

The profit from \(q\) units of output

\pi(q) = r(q) - c(q)

PROFIT

REVENUE

COST

is the revenue from selling them

minus the cost of producing them.

Revenue

We will assume that the firm sells all units of the good for the same price, \(p\). (No "price discrimination")

r(q) = p(q) \times q

The revenue from \(q\) units of output

REVENUE

PRICE

QUANTITY

is the price at which each unit it sold

times the quantity (# of units sold).

The price the firm can charge may depend on the number of units it wants to sell: inverse demand \(p(q)\)

- Usually downward-sloping: to sell more output, they need to drop their price

- Special case: a price taker faces a horizontal inverse demand curve;

can sell as much output as they like at some constant price \(p(q) = p\)

Demand and Inverse Demand

Demand curve:

quantity as a function of price

Inverse demand curve:

price as a function of quantity

QUANTITY

PRICE

\text{revenue} = r(q) = p(q) \times q

\text{marginal revenue} = {dr \over dq} = {dp \over dq} \times q + p(q)

\displaystyle{\text{average revenue} = \frac{r(q)}{q} = p(q)}

If the firm wants to sell \(q\) units, it sells all units at the same price \(p(q)\)

Since all units are sold for \(p\), the average revenue per unit is just \(p\).

By the product rule...

let's delve into this...

Total, Average, and Marginal Revenue

\text{marginal revenue} = {dr \over dq} = {dp \over dq} \times q + p

dr = dp \times q + dq \times p

p

p(q)

q

The total revenue is the price times quantity (area of the rectangle)

\text{marginal revenue} = {dr \over dq} = {dp \over dq} \times q + p

dr = dp \times q + dq \times p

p

p(q)

q

dp

dq

The total revenue is the price times quantity (area of the rectangle)

If the firm wants to sell \(dq\) more units, it needs to drop its price by \(dp\)

Revenue loss from lower price on existing sales of \(q\): \(dp \times q\)

Revenue gain from additional sales at \(p\): \(dq \times p\)

Demand

Inverse Demand

q(p) = 20 - p

p(q) = 20-q

Revenue

r(q) =

MR(q)=

AR(q)=

20q - q^2

20 - 2q

20 - q

pollev.com/chrismakler

Suppose instead that the firm faced the demand function

(not inverse demand!)

\(q(p) = 20 - 2p\).

What would their marginal revenue function \(MR(q)\) be?

Correctness matters on this one...

Demand

Inverse Demand

q(p) = 20 - p

q(p) = 20 - 2p

p(q) = 20-q

p(q) = 10 - \tfrac{1}{2}q

Revenue

r(q) =

MR(q)=

AR(q)=

r(q) =

MR(q)=

AR(q)=

20q - q^2

20 - 2q

20 - q

10q - \tfrac{1}{2}q^2

10 - q

10 - \tfrac{1}{2}q

Profit

\pi(q) = \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ -

Optimize by taking derivative and setting equal to zero:

\pi'(q) = \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ - \ \ \ \ \ \ \ \ \ = 0

\Rightarrow \ \ \ \ \ \ \ \ \ \ \ \ \ \ =

Profit is total revenue minus total costs:

"Marginal revenue equals marginal cost"

(64 + {1 \over 4}q^2)

(20q - q^2)

r'(q)

c'(q)

{1 \over 2}q

20 - 2q

r'(q)

c'(q)

{1 \over 2}q

20 - 2q

40 - 4q = q

40 = 5q

q^* = 8

CHECK YOUR UNDERSTANDING

p(q)=20-2q

c(q)=10+5q+{1 \over 2}q^2

Find the profit-maximizing quantity.

Average Profit Analysis

\pi(q) = r(q) - c(q)

Multiply right-hand side by \(q/q\):

\pi(q) = \left[{r(q) \over q} - {c(q) \over q}\right] \times q

= (AR - AC) \times q

Profit is total revenue minus total costs:

"Profit per unit times number of units"

AVERAGE PROFIT

Next Time

- How does demand elasticity affect a firm's ability to mark up its price above marginal cost?

- Extreme example: a firm facing perfectly elastic demand (i.e., a "price taker" or "competitive firm")

Econ 50 | Fall 25 | Lecture 16

By Chris Makler

Econ 50 | Fall 25 | Lecture 16

Production and Cost for a Firm