Stock Market

Trading Simulation

Stock Market

Trading Simulation

股票模擬交易-均值回歸策略

均值回歸策略

均值回歸策略

Mean Reversion Startegy

均值回歸策略

Mean Reversion Startegy

EBBS AND FLOWS

均值回歸策略

Mean Reversion Startegy

均值回歸策略

Mean Reversion Startegy

對於長遠股市我們用 0.15% 來交易

對於上漲波動股市我們用 1.5% 來交易

均值回歸策略

Mean Reversion Startegy

1.在波動市場中保持穩定

均值回歸策略

Mean Reversion Startegy

1.在波動市場中保持穩定

2.實際運用

import matplotlib.pyplot as pltfor _ in range(1, days):

change = random.uniform(-2, 2)

new_price = prices[-1] * (1 + change / 100)

prices.append(new_price)for i in range(1, days):

today = prices[i]

yesterday = prices[i-1]

change_pct = (today - yesterday) / yesterday * 100

#if ahhhhhhhhh find reset point

if change_pct < -1.5 and cash >= today:

shares += 1

cash -= today

history.append(f"Day {i}: Bought at {today:.2f}")

elif change_pct > 1.5 and shares > 0:

shares -= 1

cash += today

history.append(f"Day {i}: Sold at {today:.2f}")portfolio_value = cash + shares * prices[-1]

#剩餘的本金加股票的價值

import matplotlib.pyplot as plt問題

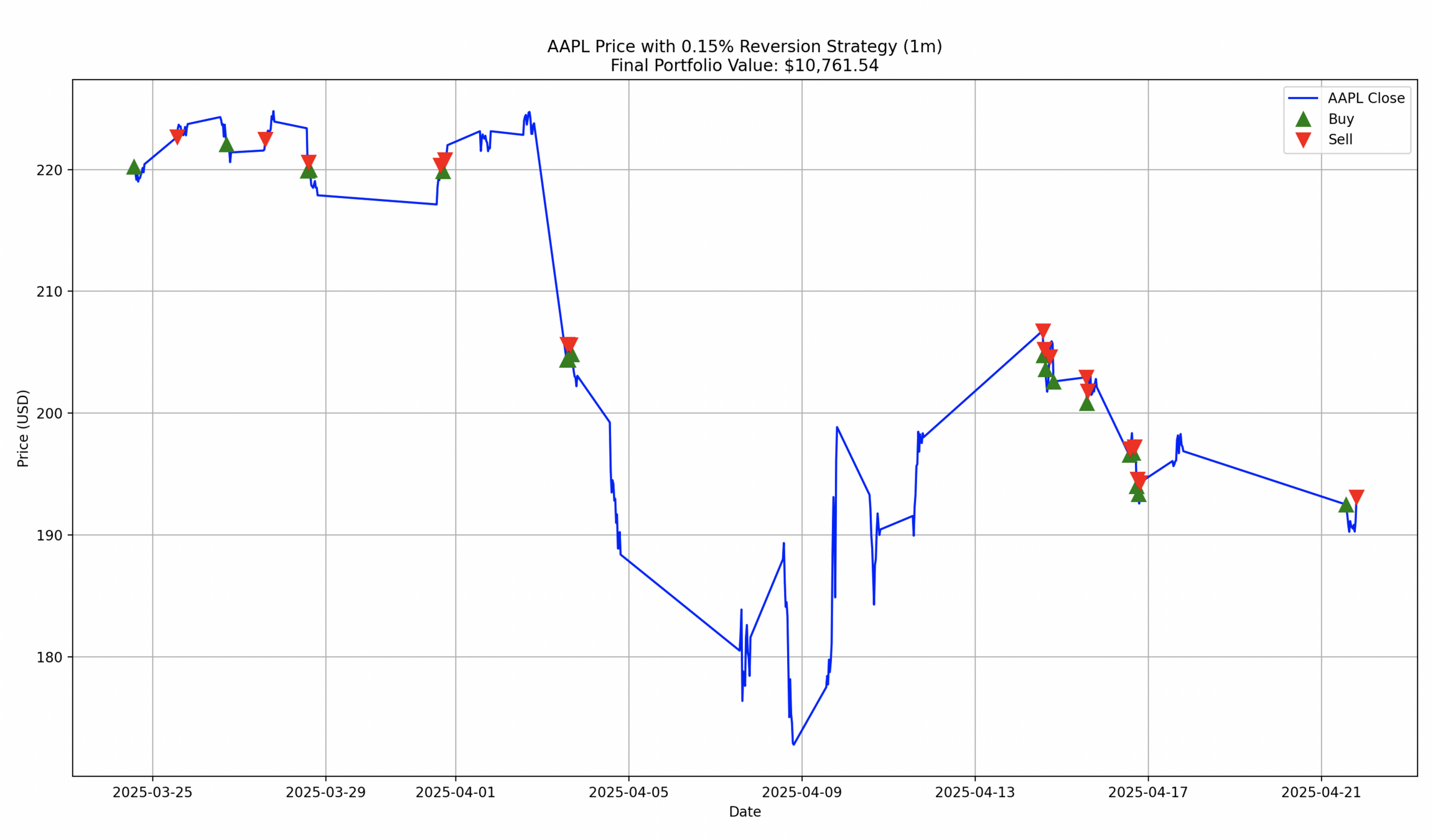

import yfinance as yf

import matplotlib.pyplot as plt

TICKER = 'AAPL'

PERIOD = '1mo'

INTERVAL = '30m'

THRESHOLD = 0.0015 # 0.15%

INITIAL_CAPITAL = 10000.0

data = yf.download(TICKER, period=PERIOD, interval=INTERVAL)

prices = data['Close'].values

dates = data.index

position = True

buy_price = float(prices[0])

sell_price = None

capital = 0.0

quantity = INITIAL_CAPITAL / buy_price

buy_signals = [dates[0]]

sell_signals = []

for i in range(1, len(prices)):

p = float(prices[i])

current_date = dates[i]

#check the reset point if avilable ahhhh no

if position:

if p >= buy_price * (1 + THRESHOLD):

sell_price = p

capital = quantity * sell_price

quantity = 0.0

position = False

sell_signals.append(current_date)

print(f"SELL at ${p:.2f} on {current_date}")

else:

if p <= sell_price * (1 - THRESHOLD):

buy_price = p

quantity = capital / buy_price

capital = 0.0

position = True

buy_signals.append(current_date)

print(f"BUY at ${p:.2f} on {current_date}")

final_value = capital + quantity * float(prices[-1])

plt.figure(figsize=(14,6))

plt.plot(dates, prices, label=f'{TICKER} Close', color='blue')

plt.plot(buy_signals, data['Close'].loc[buy_signals], '^', markersize=10, color='green', label='Buy')

plt.plot(sell_signals, data['Close'].loc[sell_signals], 'v', markersize=10, color='red', label='Sell')

plt.title(f'{TICKER} Price with 0.15% Reversion Strategy (1m)\nFinal Portfolio Value: ${final_value:,.2f}')

plt.xlabel('Date')

plt.ylabel('Price (USD)')

plt.legend()

plt.grid(True)

plt.tight_layout()

plt.show()

print(f"\nFinal Portfolio Value: ${final_value:,.2f}")

print("class dismissed!!!")import yfinance as yf

import matplotlib.pyplot as plt

TICKER = 'AAPL'

PERIOD = '1mo'

INTERVAL = '30m'

THRESHOLD = 0.0015 # 0.15%

INITIAL_CAPITAL = 10000.0

data = yf.download(TICKER, period=PERIOD, interval=INTERVAL)

prices = data['Close'].values

dates = data.index

position = True

buy_price = float(prices[0])

sell_price = None

capital = 0.0

quantity = INITIAL_CAPITAL / buy_price

buy_signals = [dates[0]]

sell_signals = []

for i in range(1, len(prices)):

p = float(prices[i])

current_date = dates[i]

#check the reset point if avilable ahhhh no

if position:

if p >= buy_price * (1 + THRESHOLD):

sell_price = p

capital = quantity * sell_price

quantity = 0.0

position = False

sell_signals.append(current_date)

print(f"SELL at ${p:.2f} on {current_date}")

else:

if p <= sell_price * (1 - THRESHOLD):

buy_price = p

quantity = capital / buy_price

capital = 0.0

position = True

buy_signals.append(current_date)

print(f"BUY at ${p:.2f} on {current_date}")

final_value = capital + quantity * float(prices[-1])

plt.figure(figsize=(14,6))

plt.plot(dates, prices, label=f'{TICKER} Close', color='blue')

plt.plot(buy_signals, data['Close'].loc[buy_signals], '^', markersize=10, color='green', label='Buy')

plt.plot(sell_signals, data['Close'].loc[sell_signals], 'v', markersize=10, color='red', label='Sell')

plt.title(f'{TICKER} Price with 0.15% Reversion Strategy (1m)\nFinal Portfolio Value: ${final_value:,.2f}')

plt.xlabel('Date')

plt.ylabel('Price (USD)')

plt.legend()

plt.grid(True)

plt.tight_layout()

plt.show()

print(f"\nFinal Portfolio Value: ${final_value:,.2f}")

print("class dismissed!!!")pip install yfinanceplt.plot

(buy_signals, data['Close'].loc[buy_signals], '^',

markersize=10, color='green', label='Buy')

plt.plot

(sell_signals, data['Close'].loc[sell_signals], 'v',

markersize=10, color='red', label='Sell')plt.plot

(buy_signals, data['Close'].loc[buy_signals], '^',

markersize=10, color='green', label='Buy')

plt.plot

(sell_signals, data['Close'].loc[sell_signals], 'v',

markersize=10, color='red', label='Sell')plt.plot

(buy_signals, data['Close'].loc[buy_signals], '^',

markersize=10, color='green', label='Buy')

plt.plot

(sell_signals, data['Close'].loc[sell_signals], 'v',

markersize=10, color='red', label='Sell')

RESET POINT

RESET POINT

本金分配

RESET POINT

本金分配 -> random 每筆投資

RAND_T

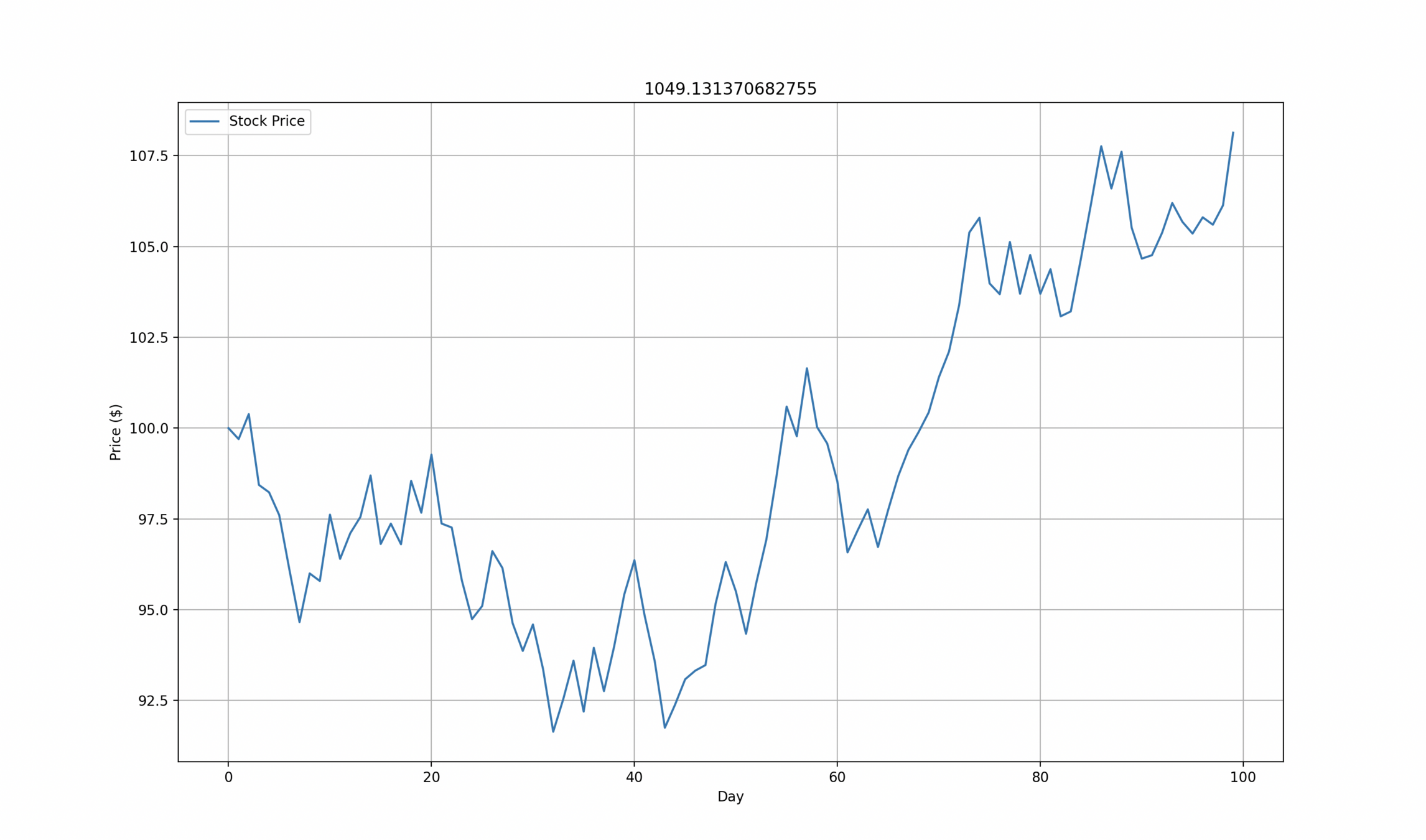

import random

import matplotlib.pyplot as plt

days = 100

initial_price = 100

prices = [initial_price]

for _ in range(1, days):

change = random.uniform(-2, 2)

new_price = prices[-1] * (1 + change / 100)

prices.append(new_price)

cash = 1000

shares = 0

history = []

for i in range(1, days):

today = prices[i]

yesterday = prices[i-1]

change_pct = (today - yesterday) / yesterday * 100

#if ahhhhhhhhh find reset point

if change_pct < -1.5 and cash >= today:

shares += 1

cash -= today

history.append(f"Day {i}: Bought at {today:.2f}")

elif change_pct > 1.5 and shares > 0:

shares -= 1

cash += today

history.append(f"Day {i}: Sold at {today:.2f}")

portfolio_value = cash + shares * prices[-1]

print("\n".join(history))

print(f"\nFinal Portfolio Value: ${portfolio_value:.2f}")

plt.plot(prices, label="Stock Price")

plt.title(portfolio_value)# i need title

plt.xlabel("Day")

plt.ylabel("Price ($)")

plt.grid(True)

plt.legend()

plt.show()APPL_1mo (0.15%)

import yfinance as yf

import matplotlib.pyplot as plt

TICKER = 'AAPL'

PERIOD = '1mo'

INTERVAL = '30m'

THRESHOLD = 0.0015 # 0.15%

INITIAL_CAPITAL = 10000.0

data = yf.download(TICKER, period=PERIOD, interval=INTERVAL)

prices = data['Close'].values

dates = data.index

position = True

buy_price = float(prices[0])

sell_price = None

capital = 0.0

quantity = INITIAL_CAPITAL / buy_price

buy_signals = [dates[0]]

sell_signals = []

for i in range(1, len(prices)):

p = float(prices[i])

current_date = dates[i]

#check the reset point if avilable ahhhh no

if position:

if p >= buy_price * (1 + THRESHOLD):

sell_price = p

capital = quantity * sell_price

quantity = 0.0

position = False

sell_signals.append(current_date)

print(f"SELL at ${p:.2f} on {current_date}")

else:

if p <= sell_price * (1 - THRESHOLD):

buy_price = p

quantity = capital / buy_price

capital = 0.0

position = True

buy_signals.append(current_date)

print(f"BUY at ${p:.2f} on {current_date}")

final_value = capital + quantity * float(prices[-1])

plt.figure(figsize=(14,6))

plt.plot(dates, prices, label=f'{TICKER} Close', color='blue')

plt.plot(buy_signals, data['Close'].loc[buy_signals], '^', markersize=10, color='green', label='Buy')

plt.plot(sell_signals, data['Close'].loc[sell_signals], 'v', markersize=10, color='red', label='Sell')

plt.title(f'{TICKER} Price with 0.15% Reversion Strategy (1m)\nFinal Portfolio Value: ${final_value:,.2f}')

plt.xlabel('Date')

plt.ylabel('Price (USD)')

plt.legend()

plt.grid(True)

plt.tight_layout()

plt.show()

print(f"\nFinal Portfolio Value: ${final_value:,.2f}")

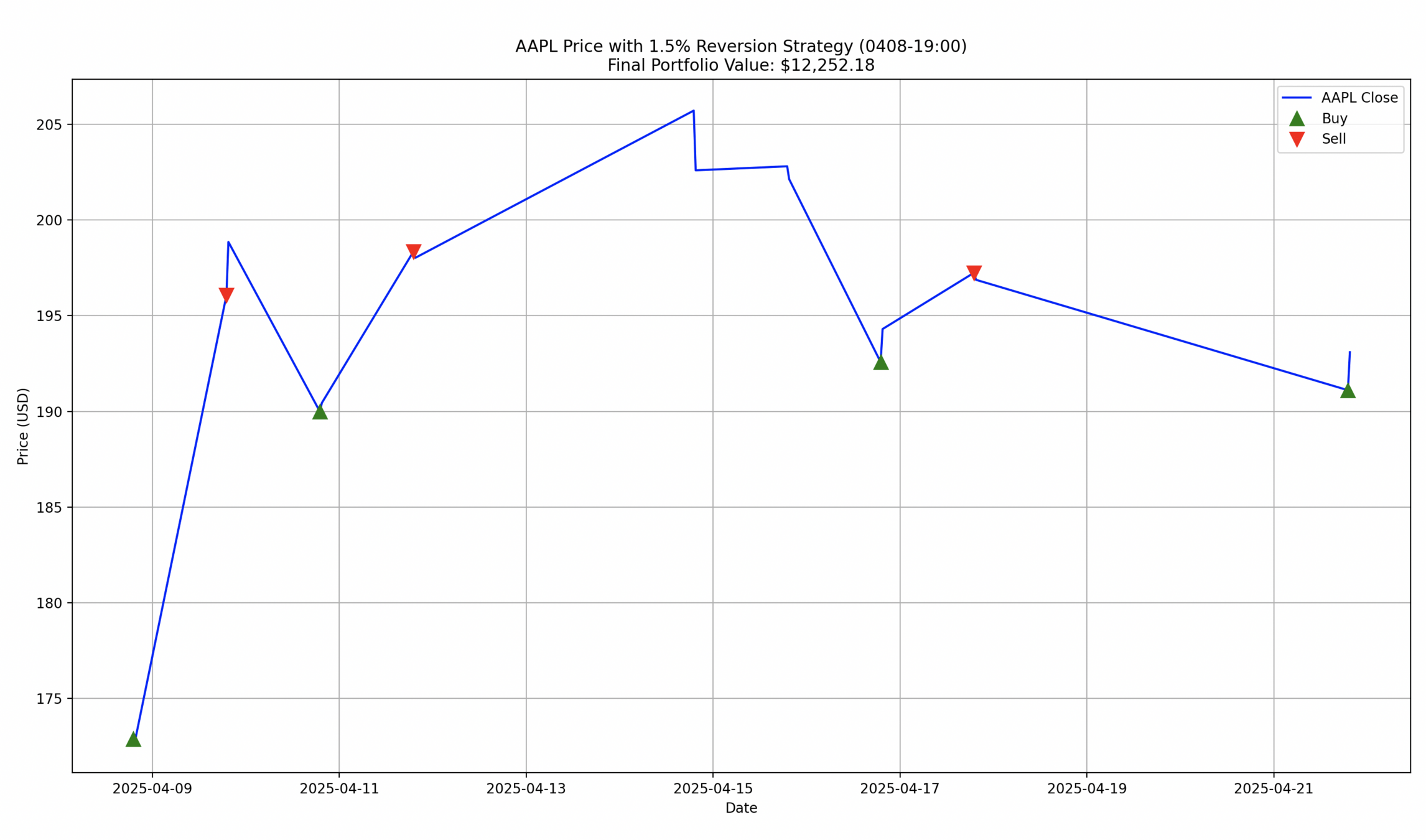

print("class dismissed!!!")APPL_4/8 (1.5%)

import yfinance as yf

import matplotlib.pyplot as plt

TICKER = 'AAPL'

PERIOD = '1mo'

INTERVAL = '30m'

THRESHOLD = 0.015 # 1.5% (adjustable)

INITIAL_CAPITAL = 10000.0

START_DATE = '2025-04-08'

data = yf.download(TICKER, start=START_DATE, period=PERIOD, interval=INTERVAL)

data = data[data.index.hour >= 19]

prices = data['Close'].values

dates = data.index

position = True

buy_price = float(prices[0])

sell_price = None

capital = 0.0

quantity = INITIAL_CAPITAL / buy_price

buy_signals = [dates[0]]

sell_signals = []

for i in range(1, len(prices)):

p = float(prices[i])

current_date = dates[i]

# Check the reset point if available(no

if position:

if p >= buy_price * (1 + THRESHOLD):

sell_price = p

capital = quantity * sell_price

quantity = 0.0

position = False

sell_signals.append(current_date)

print(f"SELL at ${p:.2f} on {current_date}")

else:

if p <= sell_price * (1 - THRESHOLD):

buy_price = p

quantity = capital / buy_price

capital = 0.0

position = True

buy_signals.append(current_date)

print(f"BUY at ${p:.2f} on {current_date}")

final_value = capital + quantity * float(prices[-1])

plt.figure(figsize=(14, 6))

plt.plot(dates, prices, label=f'{TICKER} Close', color='blue')

plt.plot(buy_signals, data['Close'].loc[buy_signals], '^', markersize=10, color='green', label='Buy')

plt.plot(sell_signals, data['Close'].loc[sell_signals], 'v', markersize=10, color='red', label='Sell')

plt.title(f'{TICKER} Price with 1.5% Reversion Strategy (0408-19:00)\nFinal Portfolio Value: ${final_value:,.2f}')

plt.xlabel('Date')

plt.ylabel('Price (USD)')

plt.legend()

plt.grid(True)

plt.tight_layout()

plt.show()

print(f"\nFinal Portfolio Value: ${final_value:,.2f}")

print("class dismissed!!!")

deck

By chen0121