Book 5. Risk and Investment Management

FRM Part 2

IM 9. Risk, Regulation, and Organizational Structure

Presented by: Sudhanshu

Module 1. Hedge Fund Risks and Systemic Risk

Module 2. Regukation and Organizational Structure

Module 1. Hedge Fund Risks and Systemic Risk

Topic 1. Risk in Hedge Fund Investing

Topic 2. Leverage

Topic 3. Regulation

Topic 4. Short Selling

Topic 5. Transparency

Topic 6. Risk Tolerance

Topic 7. Systemic Risk From Hedge Fund Activities

Topic 8. Systemic Risk From Bank Exposure to Hedge Funds

Topic 1. Risk in Hedge Fund Investing

-

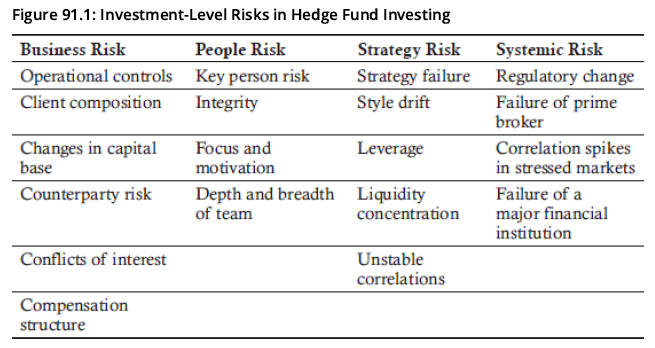

Hedge funds risks can be broadly classified into two categories: portfolio-level and investment-level risks.

-

Portfolio-Level Risks: Include benchmarking issues, survivorship bias, and unrelated business taxable income (UBTI):

-

UBTI can arise when debt-financed income becomes taxable for investors who are otherwise tax exempt.

-

Investing through an offshore hedge fund can help mitigate UBTI risk.

-

- Investment-Level Risks: Include counterparty risk, conflicts of interest, key person risk, strategy failure, style drift, regulatory changes, and correlation spikes.

Topic 1. Risk in Hedge Fund Investing

- Hedge funds risks can also be classified based on five incremental risks:

- Leverage: Amplification of both gains and losses.

- Regulation: Generally lighter oversight compared to mutual funds.

- Short Selling: Potential for unlimited downside risk and exposure to "short squeezes".

- Transparency: High levels of secrecy regarding specific trades to protect arbitrage opportunities.

- Risk Tolerance: Managers are often incentivized by compensation structures to take on higher risk.

-

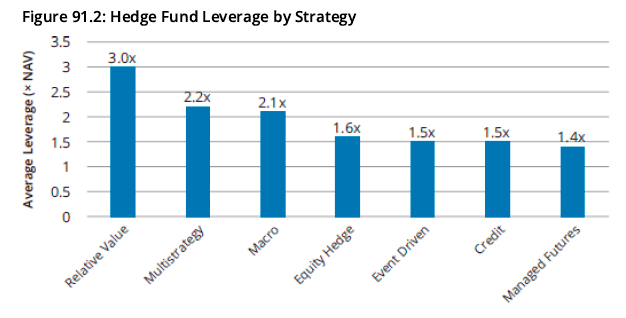

Returns Amplification: Hedge funds frequently amplify outcomes through leverage, which can take the form of:

-

On-balance-sheet: Direct borrowing of funds.

-

Off-balance-sheet: The use of derivatives.

-

-

Leverage can significantly boost gains during positive returns, but in periods of negative returns, it can equally intensify losses.

-

Leverage can also increase a hedge fund’s sensitivity to liquidity shocks.

-

Most hedge fund leverage is collateralized with cash or assets held by the fund; true uncollateralized borrowing is rare.

-

Fig 91.2 presents leverage data by strategy, based on 2020 findings.

Topic 2. Leverage

-

Limited Traditional Oversight: Hedge funds operate with significantly less regulatory oversight than open-end mutual funds, requiring investors to conduct their own due diligence.

-

United States

- Private Adviser Exemption: Under the Investment Advisers Act of 1940, hedge fund managers advising fewer than 15 clients were historically exempt from registration

- Post-Crisis Dodd-Frank Requirements (2010): Hedge fund advisers managing at least $150 million in assets must:

- Register with the Securities and Exchange Commission (SEC)

- Maintain extensive records and make them available to the SEC

- Appoint a chief compliance officer (CCO)

- Undergo periodic SEC examinations

- Indirect Regulation: Hedge funds are indirectly regulated through their highly regulated counterparties, particularly banks

Topic 3. Regulation

-

European Union - AIFMD (2010): Alternative Investment Fund Managers Directive established comprehensive hedge fund and private equity regulations including:

- Mandatory registration requirements

- Limits on leverage

- Detailed reporting, disclosure, and marketing rules for EU and non-EU funds

- European Securities and Markets Authority (ESMA) created in 2011 to interpret provisions, with enforcement by individual member states

- Singapore (2010): Hedge funds exceeding $250 million in assets must:

- Register with the Monetary Authority of Singapore (MAS)

- Provide quarterly unaudited and annual audited reports to investors and MAS

- Obtain capital markets services license from MAS

- Hong Kong - Securities and Futures Ordinance:

- Defines hedge fund activities to include securities dealing, leveraged foreign exchange trading, and futures contracts

- Requires licenses corresponding to specific business activities

- Outlines recommended reporting and disclosure practices

- Places limits on marketing efforts to potential clients

Topic 3. Regulation

-

China - Distinctive Framework:

- Funds classified as government-supported or private (private segment in early development stage)

- China Securities Regulatory Commission (CSRC) as primary regulator

- Prohibits leverage use and restricts short selling to only 50 securities on CSI 300 Index

- Brokers cannot use client shares for short sales, making shorting expensive (~10% annually)

- China Insurance Regulatory Commission (CIRC) encourages insurance companies to establish asset management firms for hedge fund-like strategies

Topic 3. Regulation

| Jurisdication | Key Regulatory Body/ Act | Core Requirements & Restrictions |

|---|---|---|

| European Union | AIFMD & ESMA | Mandatory registration, limits on leverage, and detailed reporting/disclosure rules. |

| Singapore | Monetary Authority of Singapore (MAS) | Funds with >$250 million in assets must register, obtain a capital markets services license, and provide quarterly unaudited/annual audited reports. |

| Hing Kong | Securities and Futures Ordinance (SFO) | Defines specific licensed activities (e.g., leveraged FX trading) and outlines recommended disclosure practices. |

| China | CSRC | Strict Prohibition: The use of leverage is prohibited, and short selling is restricted to only 50 securities on the CSI 300 Index |

Practice Questions: Q1

Q1. Hedge funds encounter the most significant restrictions on short selling in which of the following jurisdictions?

A. China.

B. Singapore.

C. Hong Kong.

D. The European Union.

Practice Questions: Q1 Answer

Explanation: A is correct.

Short selling in China is heavily restricted. Only 50 securities in the CSI 300 Index may be shorted, and brokers cannot use client shares to facilitate short sales. This makes shorting extremely costly, at roughly 10% per year.

-

Beyond leverage and regulation, hedge funds face unique risks stemming from their specific investment strategies and management styles. These risks emerge due to:

-

short selling,

-

transparency and

-

risk tolerance.

-

-

Short Selling: Involves borrowing shares, posting collateral, adding additional collateral as required, and eventually repaying the borrowed shares when the position is closed.

-

Unlimited Downside: While long positions have limited downside because financial assets cannot have negative values, short positions have theoretically unlimited downside risk because a stock's price has no upper bound.

-

Short Squeeze: This occurs when a heavily shorted stock's price rises rapidly, forcing short sellers to buy shares to close their positions, which further accelerates the price increase.

-

Real-World Example: The 2021 GameStop (GME) event serves as a prominent example of a short squeeze.

-

Topic 4. Short Selling

-

Transparency: Hedge funds are known for being secretive, which creates a specific "transparency risk" for investors trying to monitor their portfolios.

-

Secretive Strategies: Funds often keep strategies private to prevent "crowded trades," where too many participants arbitrage the same inefficiency, causing the profit opportunity to disappear.

-

Monitoring Challenges: This lack of transparency makes it difficult for investors to evaluate risk or ensure the manager is staying aligned with the agreed-upon strategy.

-

Liquidity Restrictions: Exit gates and other liquidity limitations can trap investors who become concerned about "style drift" or strategy shifts but cannot immediately withdraw capital.

-

Topic 5. Transparency

-

Risk Tolerance: Hedge fund managers typically exhibit a much higher risk tolerance than mutual fund managers.

-

Incentive Structures: Performance-based compensation often incentivizes managers to take on additional risk to reach high-water marks or maximize gains.

-

Complex Instruments: Managers frequently use derivatives and innovative strategies. While these can mitigate some risks, they introduce complexities that make overall risk assessment more difficult for the investor.

-

Topic 6. Risk Tolerance

-

Systemic Risk: The threat of disruption to the broader financial system or the overall economy. Hedge funds contribute to this risk primarily through two channels:

- Contagion Through Strategy Failure: Hedge fund failures can trigger broader financial disruption when funds are forced to unwind positions at fire sale prices, spreading distress across markets

- Counterparty Risk to Financial Institutions: Hedge funds can impose large losses on banks and other financial institutions that serve as lenders or counterparties

- Case Study 1: Long-Term Capital Management (1998):

- Demonstrated that typically independent assets can become highly correlated and move in the same direction during extreme market stress

- Underscored critical importance of monitoring liquidity and leverage

- Case Study 2: Amaranth Advisors (2006):

- Raised questions about systemic risk posed by hedge funds

- Bank of England concluded key intermediaries (banks) contributed more to systemic risk than hedge funds themselves

- Suggested hedge funds may facilitate risk transfer in ways that reduce systemic risk

- Critics counter that hedge fund leverage and complex, nonlinear strategies can increase systemic risk

Topic 7. Systemic Risk From Hedge Fund Activities

-

Mechanics of Systemic Contagion:

-

Forced Deleveraging Spiral: During the Global Financial Crisis, lenders forced hedge funds to post additional collateral and unwind positions, creating fire sales that caused contagion and losses in otherwise uncorrelated asset classes

- Amplification Factors:

- Leverage magnifies selling pressure

- Computer-driven algorithmic selling accelerates declines

- Margin calls from counterparties trigger forced liquidations

- Investor redemptions increase selling pressure

- Declining risk appetite during market stress compounds effects

- Fund of Funds Cascade: Redemptions from funds of hedge funds cascade to underlying hedge funds, creating a waterfall effect of additional forced selling

-

Topic 7. Systemic Risk From Hedge Fund Activities

-

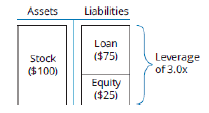

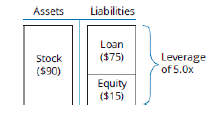

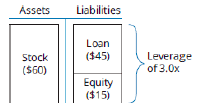

Leverage-Driven Selling Example:

-

Note that:

-

-

Initial Position: Hedge fund owns $100 stock with 25% margin (3x leverage: $75 borrowed, $25 equity)

- Price Decline Impact: 10% stock price fall to $90 increases leverage to 5x ($75 loan unchanged, equity falls to $15)

- Forced Deleveraging: To restore 3x leverage, fund must sell $30 of stock despite no fundamental reason for selling

- Downward Spiral: As asset prices decline further, increasingly large position liquidations become necessary to meet leverage requirements, creating a self-reinforcing cycle of selling and price declines

-

Topic 7. Systemic Risk From Hedge Fund Activities

Initial Position

Price Decline

Forced Deleveraging

Practice Questions: Q2

Q2. Which of the following actions is least likely to reduce systemic risk associated with hedge funds?

A. Strict new regulations.

B. Lower leverage in hedge fund portfolios.

C. More conservative lending practices by banks.

D. Greater diversification in hedge fund portfolios.

Practice Questions: Q2 Answer

Explanation: A is correct.

Measures that help mitigate systemic risk include conservative lending standards by banks, lower leverage in hedge fund portfolios, and greater diversification. While reasonable regulation can play a role, overly strict regulation may reduce market liquidity and could actually increase systemic risk.

-

Primary Risks: Banks face three primary types of risk while engaging with hedge funds:

-

Revenue Risk: Banks earn significant fee and service income from hedge funds through trading, clearing, custody, securities lending, financing, and reporting activities. The failure of multiple hedge funds could materially reduce this revenue stream.

-

Credit Risk: Margin loans are secured by collateral, but the value of the underlying assets can decline more quickly than anticipated, potentially leaving the bank undersecured.

-

Counterparty Risk: Banks face exposure through derivatives transactions with hedge funds, such as credit default swaps (CDSs) and other over-the-counter (OTC) contracts.

-

-

The Case of Archegos Capital (2021): The collapse of Archegos Capital serves as a primary example of how concentrated, leveraged exposure can threaten the banking sector.

-

Mechanism: Although a family office, Archegos used total return swaps to create exposures identical to hedge fund leverage.

-

Impact: The default resulted in a loss of approximately $5 billion for Credit Suisse and another $5 billion collectively for other banks.

-

Consequence: This failure led banks to tighten requirements, forcing hedge funds to reduce leverage to protect the systemic health of the sector.

-

Topic 8. Systemic Risk From Bank Exposure to Hedge Funds

-

Systemic Risk Mitigation Strategies: There are three core approaches to reducing the systemic impact of hedge funds:

-

Conservative Lending: Banks must adopt more stringent lending practices.

-

Portfolio Management: Hedge funds should maintain lower leverage and higher diversification.

-

Reasonable Regulation: Oversight should be balanced; however, the text notes that "excessively strict regulation" could harm markets by reducing the liquidity hedge funds provide as "investors of last resort".

-

Topic 8. Systemic Risk From Bank Exposure to Hedge Funds

Module 2. Regulation and Organizational Structure

Topic 1. U.S. Regulatory Framework

Topic 2. European Hedge Fund Regulation

Topic 3. Regulatory Objectives and Industry Self-Regulation

Topic 4. Organizational and Structural Design

Topic 5. Tax Motivations and Regulatory Considerations

Topic 1. U.S. Regulatory Framework

-

Investment Company Act of 1940 ('40 Act) Exemptions

-

Registration Avoidance: Mutual funds must register with SEC (regular reporting, limits on leverage, short selling, performance fees); hedge funds avoid registration through two exemptions:

- Section 3(c)(1): Exemption for funds with fewer than 100 investors

- Section 3(c)(7): Exemption for funds limited to qualified purchasers (individuals with >$5 million in investment assets); must register under '34 Act if 500+ investors

-

-

Additional Regulatory Exemptions

- Investment Advisers Act (1940) - Private Adviser Exemption: Managers exempt if advising fewer than 15 funds; many firms structure to stay below this threshold

- ERISA Compliance: Hedge funds avoid Employee Retirement Income Security Act requirements by limiting benefit plan participation to <25% of total fund assets

- Regulation D (Reg D) - Private Placements

- Marketing Restrictions: Hedge funds use private placements rather than public offerings; cannot advertise to general public

- Investor Requirements: Only accredited investors allowed (net worth ≥$2.5 million OR annual income ≥$250,000 for prior two years); Rule 506 permits up to 35 nonaccredited investors

Topic 1. U.S. Regulatory Framework

-

Historical Regulatory Evolution

- 2004-2006: SEC attempted mandatory hedge fund registration; overturned by U.S. Court of Appeals for D.C. in 2006

- 2007: President's Working Group rejected broad regulation; encouraged voluntary industry guidelines

- Post-2008: Madoff fraud and Global Financial Crisis renewed regulatory scrutiny

- Dodd-Frank Act (2010) - Title V

- Private Fund Investment Advisers Registration Act: Eliminated private adviser exemption; former "15-client" threshold no longer relevant; hedge fund managers now required to register with SEC

- Reporting Requirements: Mandatory submissions to SEC and Financial Stability Oversight Council (FSOC) covering AUM, leverage, counterparty exposures, and investment strategies

- Form PF: Detailed operational and portfolio information filing:

- Annual: Advisers with ≥$150 million AUM

- Quarterly: Advisers with >$1.5 billion AUM

Practice Questions: Q1

Q1. Which of the following regulations requires U.S.-based hedge fund managers to register with the SEC?

A. Regulation D.

B. Title IV of the Dodd-Frank Act.

C. Investment Advisers Act of 1940.

D. Alternative Investment Fund Managers Directive.

Practice Questions: Q1 Answer

Explanation: B is correct.

Title IV of the Dodd-Frank Act eliminated the private adviser exemption under the Investment Advisers Act of 1940. Before Dodd-Frank, hedge fund managers could avoid SEC registration if they advised fewer than 15 funds. Regulation D governs private placements and accredited investor requirements, while the Alternative Investment Fund Managers Directive is an EU regulatory framework.

Topic 2. European Hedge Fund Regulation

- Restrictive Regulatory Approach: Europe has adopted a more restrictive approach to hedge fund oversight compared to the United States and United Kingdom

- Reporting Requirements for Large Funds: Hedge funds managing over €100 million in AUM face extensive reporting requirements covering:

- Leverage levels

- Investment strategies

- Risk exposures

- Marketing activities

- EU Passport Benefits: EU-domiciled hedge funds benefit from the EU Passport, facilitating easier fund management and marketing across member states

- Market Practice Regulations: European regulators have imposed additional requirements including:

- Disclosure of net short positions

- Restrictions on naked short selling

- Mandatory central clearing for derivatives transactions

- Comprehensive reporting of all derivatives trades

- Measures to slow high-frequency trading

- Country-Specific Variations: Oversight differs by jurisdiction with Portugal emphasizing derivatives market regulation, France focusing on leverage limits, and Germany restricting bank lending to highly leveraged investment vehicles including hedge funds

Topic 3. Regulatory Objectives and Industry Self-Regulation

-

Regulatory Objectives: At a high level, regulators are focused on three main concerns:

- Investor Protection: Regulators ensure hedge funds do not defraud investors by restricting participation to sophisticated investors presumed capable of evaluating hedge fund risks

- Market Integrity: Regulators monitor hedge funds for insider trading using the same rules and enforcement mechanisms applied across financial markets

- Financial Stability: Regulators prevent market destabilization by hedge funds through measures limiting leverage and requiring timely and accurate collateral posting

- Self-Regulation:

- Industry Self-Regulation: The Alternative Investment Management Association supports self-regulation by publishing the Guide to Sound Practices for Hedge Fund Valuation

- Public Listing Transparency: When hedge fund managers become publicly traded (e.g., Man Group in London, Blackstone in the United States), increased public scrutiny and transparency provide investors with more information and indirect access to the industry

Topic 4. Organizational and Structural Design

-

Domicile Selection

- Strategic Location Choices: Hedge funds select domiciles to minimize taxes and reduce regulatory oversight

- United States: Delaware is common due to favorable legal environment

- Offshore Locations: Cayman Islands (55%), British Virgin Islands (15%), Bermuda (10%)

- Tax Implications: While domicile reduces fund-level taxes, managers still pay taxes on fees earned and investors remain subject to taxation on gains in their home jurisdictions

- Strategic Location Choices: Hedge funds select domiciles to minimize taxes and reduce regulatory oversight

-

Legal Structure

- Limited Partnership: Typical legal entity structure with hedge fund manager as general partner and investors as limited partners

- Open-Ended Partnership: Allows issuance of new shares to incoming investors and redemption for exiting investors, subject to lockups and gates in the partnership agreement

Topic 4. Organizational and Structural Design

-

Master-Feeder Structure

- Purpose: Avoids multiple layers of taxation and enables tax-exempt investors to participate efficiently

- Master Fund: Central pooling vehicle where all capital is aggregated and trading activity occurs

- Feeder Funds: Multiple feeders designed for different investor groups

- Onshore Feeder: For domestic investors

- Offshore Feeder: For non-U.S. investors and U.S. tax-exempt investors (e.g., pension funds)

-

Operational Support Requirements

- Professional Services: Accountants, lawyers, auditors, administrators, and independent valuation professionals for NAV determination

- Prime Broker Services: Provides lending, counterparty services, trade execution, clearing, and settlement

Topic 5. Tax Motivations and Regulatory Considerations

- 2-and-20 Fee Structure Tax Treatment:

- Management fees (2%): Taxed as ordinary income

- Performance fees/carried interest (20%): Taxed at lower capital gains rate if underlying assets held for at least one year

- Carried interest loophole reduces manager's tax liability by approximately half compared to ordinary income rates

- Historical Tax Deferral (Pre-2008):

- Managers could defer taxation on management fees under Internal Revenue Code Section 457

- Allowed postponement of fee receipt to later tax years, managing timing of tax obligations

- This loophole was eliminated in 2008

- Ongoing Legislative Risk:

- Multiple attempts to eliminate carried interest loophole have failed (2008, 2021 under Biden Administration)

- Provision remains in place currently but subject to potential future changes

- Area of close monitoring for hedge fund managers due to legislative uncertainty

Practice Questions: Q2

Q2. Which of the following is most likely an incentive for hedge funds to be structured as limited partnerships?

A. Management fees are taxed at capital gains rates.

B. Performance fees can be taxed at capital gains rates.

C. All fees paid to the general partner are treated as capital gains.

D. Management fees can be deferred indefinitely for tax purposes.

Practice Questions: Q2 Answer

Explanation: B is correct.

Management fees are taxed as ordinary income and can no longer be deferred under Section 457, a provision eliminated in 2008. Performance fees, however, may be taxed at the lower capital gains rate if the underlying assets that generated the gains were held for at least one year. This favorable tax treatment, known as the carried interest loophole, is a key incentive for hedge funds to use the limited partnership structure.